Financial Statements

2024 Complete Audited Financial Statement

2024 Statement of Financial Position

2023 Statement of Financial Position

2022 Statement of Financial Position

2021 Statement of Financial Position

Waterworks Financial Information

Amortization of assets related to the municipal waterworks. Interest on any debt associated with the municipal waterworks. Regular expenses such as wages and supplies associated with the municipal waterworks

Purchases of capital assets. Payment of debt associated with the municipal waterworks.

2024 Public Reporting on Municipal

Waterworks :

Total waterworks revenues (R) - $450,207 Total waterworks expenses (E) - $490,095

Waterworks rate bylaw (or visit our bylaw page HERE) 2023 waterworks financial overview as per the above. Current reserves.

2023 Waterworks Financial Overview

2022 Waterworks Financial Overview

Budget

What exactly is the Village budget & how is it determined?

The Municipalities Act

A budget identifies priorities as determined by Council; A budget is a tool to communicate those priorities to the public and to staff; and A budget assists with determining whether existing financial resources are sufficient to meet municipal spending needs.

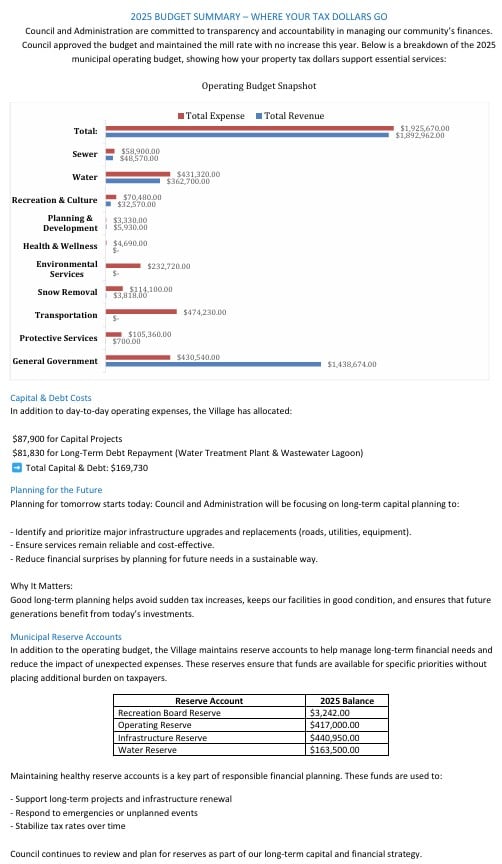

2025 Budget Overview